What Is a 401k? How It Works, Limits, and Employer Match

Most people know they should contribute to their 401k. Fewer understand how it actually works, what the limits are, or how much their employer match is really worth. Even fewer connect their daily spending habits to their ability to maximize contributions.

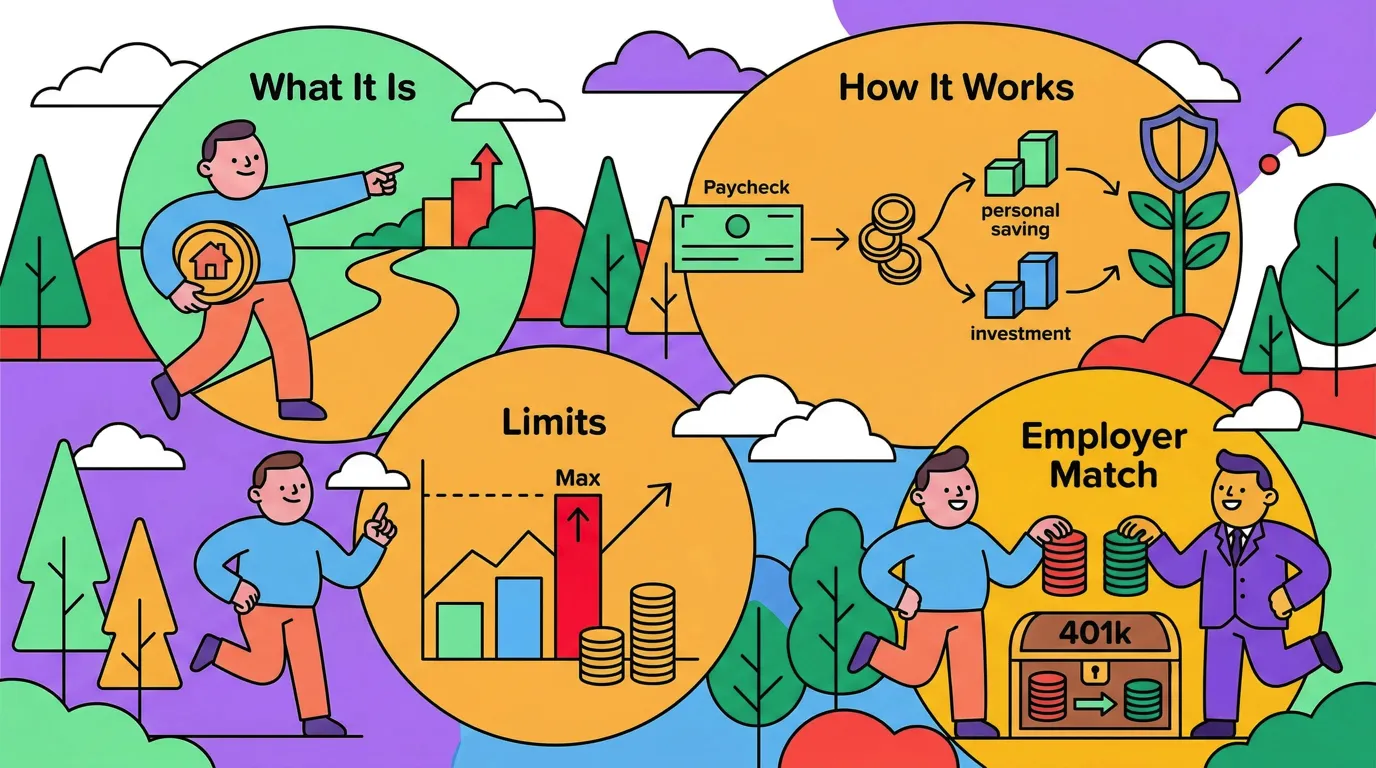

A 401k is an employer-sponsored retirement savings plan that lets you contribute pre-tax or after-tax income toward investments that grow tax-advantaged until retirement. It is one of the most powerful wealth-building tools available to employees, especially when your employer matches contributions. For a complete overview of managing your finances, see our personal finance guide.

How a 401k Works

When you enroll in a 401k, a percentage of each paycheck is automatically directed into your retirement account before you receive your pay. You choose how much to contribute (up to annual limits) and select from a menu of investment options provided by your plan.

The money grows tax-deferred, meaning you do not pay taxes on gains, dividends, or interest until you withdraw the funds in retirement. This tax deferral allows your investments to compound faster than they would in a taxable account.

The Contribution Process

- You elect a contribution percentage or dollar amount through your employer's benefits portal.

- Each pay period, that amount is deducted from your paycheck before income taxes are calculated (for traditional 401k) or after taxes (for Roth 401k).

- The funds are invested according to your selections.

- Your employer may add a matching contribution on top of yours.

2026 Contribution Limits

| Limit Type | Under 50 | Age 50+ | Age 60-63 |

|---|---|---|---|

| Employee contribution | $23,500 | $31,000 | $34,750 |

| Employer + employee total | $70,000 | $77,500 | $81,250 |

These limits increase periodically with inflation. The employee contribution limit is the most relevant number for most people. If you cannot max it out, contributing enough to capture the full employer match is the priority.

Employer Match: Free Money You Should Not Leave Behind

An employer match is additional money your company contributes to your 401k based on your own contributions. Common match structures include:

- Dollar for dollar up to 3%: If you earn $80,000 and contribute 3% ($2,400), your employer adds $2,400.

- 50 cents per dollar up to 6%: If you contribute 6% ($4,800), your employer adds $2,400.

- Flat percentage: Some employers contribute a fixed percentage regardless of your contribution.

Approximately 25% of employees with access to a 401k match do not contribute enough to get the full match. That is money left on the table. Even a 3% match on an $80,000 salary is $2,400 per year, which compounds to over $100,000 in 20 years at a 7% return.

Traditional 401k vs Roth 401k

| Feature | Traditional 401k | Roth 401k |

|---|---|---|

| Tax on contributions | Pre-tax (reduces taxable income now) | After-tax (no deduction now) |

| Tax on withdrawals | Taxed as ordinary income | Tax-free |

| Best if you expect | Lower tax rate in retirement | Higher tax rate in retirement |

| Required minimum distributions | Yes, starting at age 73 | Yes, but can roll to Roth IRA to avoid |

| Income limits | None | None |

If you are early in your career and expect your income to grow, the Roth 401k often makes sense because you pay taxes at today's lower rate. If you are in your peak earning years, the traditional 401k's immediate tax deduction may be more valuable.

Many plans allow you to split contributions between both types.

Vesting Schedules

Your own contributions are always 100% yours. But employer matching contributions may be subject to a vesting schedule, meaning you only own a percentage of the match based on how long you stay with the company.

Common vesting schedules:

- Immediate vesting: The match is fully yours right away.

- Cliff vesting: 0% until a set date (often 3 years), then 100%.

- Graded vesting: Ownership increases each year (e.g., 20% per year over 5 years).

Understanding your vesting schedule matters if you are considering leaving your job. Unvested employer contributions are forfeited when you leave.

Investment Options in a 401k

Most 401k plans offer a selection of mutual funds and target-date funds. Common options include:

- Target-date funds: Automatically adjust from aggressive to conservative as you approach retirement. Good for hands-off investors.

- Index funds: Track a market index like the S&P 500. Typically have the lowest fees in the plan.

- Bond funds: Lower risk, lower return. Used for diversification.

- Company stock: Some plans offer employer stock at a discount. Be cautious about concentration risk.

The most important factor to check is the expense ratio on each fund. A 1% difference in fees can cost tens of thousands of dollars over a career. For more on how fees affect returns, see our guide on expense ratios.

Fees to Watch

401k plans carry administrative fees that reduce your returns over time. Look for:

- Expense ratios on investment options (prefer under 0.20% for index funds)

- Plan administration fees (sometimes covered by employer, sometimes deducted from your account)

- Advisory fees if the plan includes managed account services

If your plan's fees are high and the investment options are limited, contributing enough to get the full match and then directing additional savings to an IRA may be a better strategy.

How Expense Tracking Helps You Maximize Your 401k

The biggest barrier to increasing 401k contributions is not knowing where your money goes. If you do not track spending, you cannot identify where to cut to free up more for retirement.

Here is a practical approach:

- Track all expenses for one month. Use AI-assisted input to make logging fast. Type "lunch $12" or scan a receipt, and your spending data builds itself.

- Identify discretionary spending. Categories like dining out, subscriptions, and impulse purchases are where flexibility lives.

- Redirect savings to your 401k. If you find $200 per month in reducible spending, increasing your 401k contribution by that amount adds $2,400 per year to your retirement savings.

The connection between daily spending awareness and retirement readiness is direct. Every dollar you understand in your budget is a dollar you can intentionally allocate, whether to living expenses, debt payoff, or your 401k.

For more on building this tracking habit, see our guide on how to track daily spending.

Common 401k Mistakes

Not contributing enough to get the full match. This is the highest-return, zero-risk action available. Always contribute at least enough for the full match.

Cashing out when changing jobs. A 401k withdrawal before age 59.5 triggers income tax plus a 10% penalty. Roll it over to an IRA or your new employer's plan instead.

Ignoring investment allocation. The default option may not match your risk tolerance or timeline. Review your selections at least once a year.

Not increasing contributions over time. When you get a raise, increase your 401k percentage before lifestyle creep absorbs the extra income. Even a 1% annual increase makes a significant difference over decades.

The Bottom Line

A 401k is one of the most tax-efficient ways to build retirement wealth, especially when your employer offers a match. The key is to contribute consistently, choose low-fee investment options, and increase your contribution rate over time.

The practical challenge is finding room in your budget to contribute more. That is where expense tracking becomes a retirement planning tool, not just a budgeting exercise. When you know exactly where your money goes, you can make informed decisions about how much to direct toward your future.

Common Questions About 401k Plans

How much should I contribute to my 401k?

At minimum, contribute enough to capture your full employer match. Beyond that, aim for 10-15% of gross income if possible. If you cannot reach that immediately, start where you can and increase by 1% each year.

What happens to my 401k if I leave my job?

You can leave it in your former employer's plan, roll it over to your new employer's 401k, roll it over to an IRA, or cash it out (not recommended due to taxes and penalties).

Can I withdraw from my 401k before retirement?

Yes, but withdrawals before age 59.5 typically incur a 10% early withdrawal penalty plus income tax. Some plans allow hardship withdrawals or loans, but these should be last resorts.

Is a 401k better than an IRA?

They serve different purposes and work well together. A 401k offers higher contribution limits and employer matching. An IRA offers more investment choices and potentially lower fees. Many people contribute to both.

Should I choose traditional or Roth 401k?

If you expect to be in a higher tax bracket in retirement than you are now, choose Roth. If you expect a lower bracket, choose traditional. If unsure, splitting between both provides tax diversification.

Want to find more room in your budget for retirement contributions?

Download Finny to track daily expenses with AI-assisted input. See exactly where your money goes, identify savings opportunities, and make every dollar work toward your financial goals.