Most people have a rough sense of where their money goes each month. Rent, groceries, subscriptions, the occasional dining out. But when asked to name exactly how much they spent last month, and on what, the picture gets blurry fast. That gap between what you think you spend and what you actually spend is the problem expense tracking solves.

Expense tracking is the practice of recording, categorizing, and reviewing your spending over time. It gives you a factual picture of your financial habits rather than an estimated one. Whether you use a notebook, a spreadsheet, or an AI-assisted expense tracker, the core goal is the same: know where your money goes so you can make better decisions about where it should go.

For a step-by-step approach to getting started, see our guide on how to track expenses.

What Expense Tracking Actually Means

Expense tracking is the systematic recording of money you spend. Every purchase, bill payment, transfer, or cash withdrawal gets logged with at least three pieces of information: the amount, the category, and the date. Some people also record the payment method, merchant, and notes for context.

The purpose is not just record-keeping. Tracking creates a feedback loop. When you see that you spent $480 on dining out last month, you can decide whether that number aligns with your priorities. Without tracking, that $480 disappears across dozens of small transactions that never feel significant in the moment.

Expense tracking differs from budgeting, though the two work together. A budget is a plan for future spending. Expense tracking is a record of past spending. The record informs the plan, and the plan gives the record context. You need both, but tracking comes first because you cannot create a realistic budget without knowing your actual spending patterns.

A Brief History: From Ledger Books to AI

People have tracked expenses for centuries. Merchants in medieval Europe kept handwritten ledgers. Households in the early 1900s used cash envelope systems, physically dividing money into labeled containers for rent, food, and savings.

The spreadsheet era brought expense tracking to personal computers in the 1980s and 1990s. Software like Quicken let individuals categorize transactions digitally for the first time. Then came bank-linked apps in the 2010s, which automated the process by pulling transaction data directly from financial institutions.

Each generation of tools reduced friction, but also introduced tradeoffs. Ledgers were accurate but tedious. Spreadsheets were flexible but required manual entry. Bank-linked apps were automatic but raised privacy concerns and often miscategorized transactions without user input.

Today, AI-assisted tracking represents the latest evolution. Instead of requiring you to manually enter every field or surrendering your bank credentials, AI can parse natural language input, scan receipts, and suggest categories while keeping you in control of the final record. The friction that made traditional tracking unsustainable for most people is finally being addressed without sacrificing accuracy or privacy.

Methods of Expense Tracking

There is no single correct way to track expenses. The right method depends on how much time you want to invest, how much control you need, and how comfortable you are with technology. Here are the three main approaches.

Manual Tracking

Manual tracking means recording every expense by hand, whether in a physical notebook, a spreadsheet, or a basic app. You enter the amount, category, and date yourself.

Strengths: Complete control over categorization. No privacy concerns from bank connections. Forces awareness of every purchase.

Weaknesses: Time-consuming. Easy to forget transactions. Most people abandon manual tracking within a few weeks because the effort outweighs the perceived benefit.

Manual tracking works best for people who enjoy the ritual of recording expenses and have the discipline to do it consistently. For everyone else, the dropout rate is high.

Automatic Tracking

Automatic tracking relies on bank connections or credit card syncing to import transactions. Apps pull your data, categorize it using algorithms, and present spending summaries.

Strengths: Low effort after initial setup. Captures every transaction automatically. Good for people who use cards exclusively.

Weaknesses: Requires sharing bank credentials. Often miscategorizes transactions. Does not capture cash spending. Limited control over how expenses are classified.

Automatic tracking trades control for convenience. If you primarily use one or two cards and do not mind sharing financial access, it can work. But the miscategorization problem means you still need to review and correct entries regularly.

Hybrid (AI-Assisted) Tracking

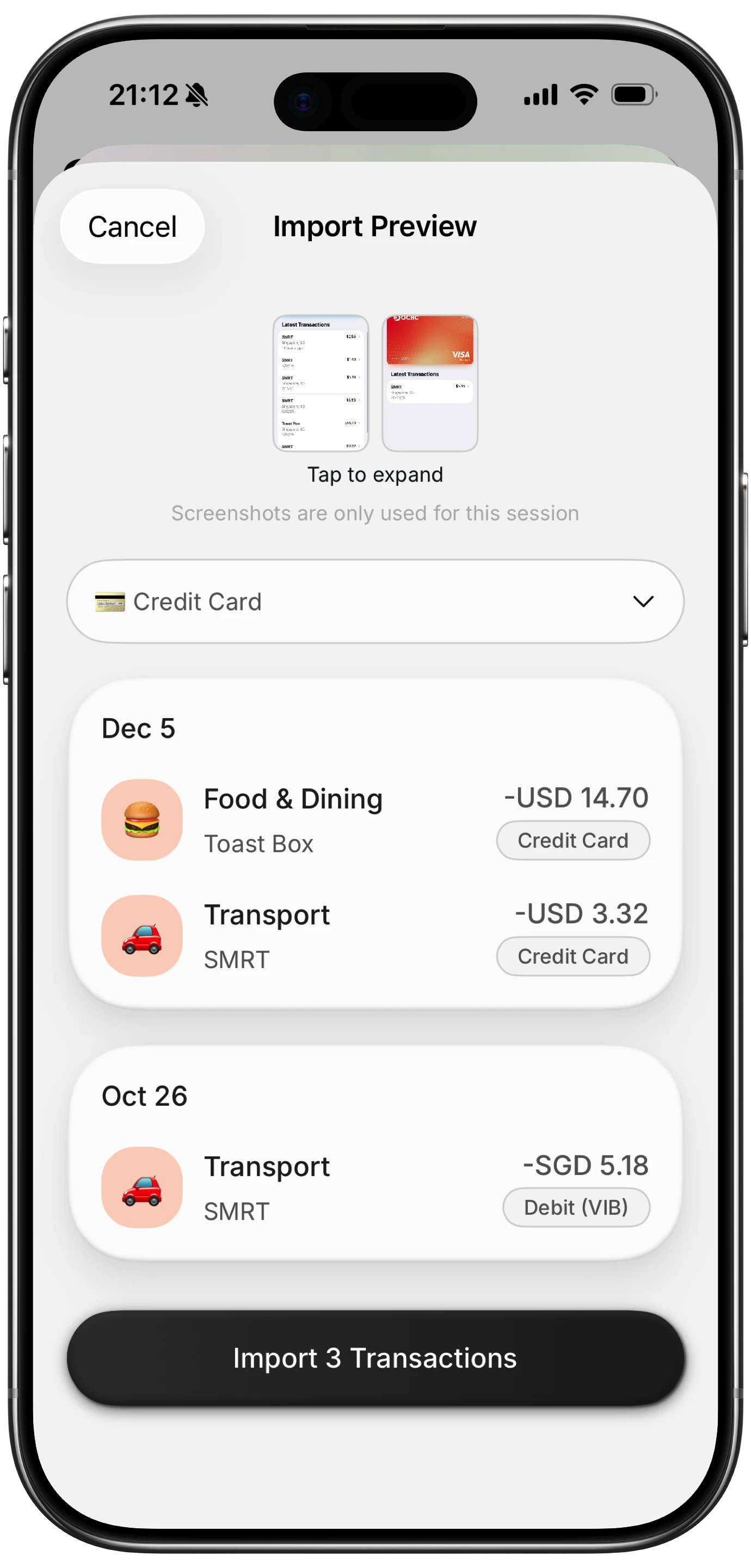

Hybrid tracking combines the accuracy of manual input with the speed of automation. You provide the input, whether by typing, speaking, or scanning a receipt, and AI handles the tedious parts like parsing amounts, suggesting categories, and formatting the entry.

Strengths: Fast input without sacrificing accuracy. No bank connections needed. Works offline. You stay in control while AI reduces friction.

Weaknesses: Still requires you to initiate each entry (though this takes seconds rather than minutes).

This is the approach Finny uses. You type "coffee 4.50" or scan a receipt, and the app handles the rest. You confirm the category and save. The process takes a few seconds per transaction, which is fast enough to be sustainable but deliberate enough to keep you aware of your spending. For a deeper comparison, see our guide on the best way to track expenses.

What You Should Track

Not every financial movement needs the same level of detail. Here is what to focus on:

Essential Categories

- Fixed expenses: Rent or mortgage, insurance, loan payments, subscriptions

- Variable necessities: Groceries, utilities, transportation, healthcare

- Discretionary spending: Dining out, entertainment, shopping, hobbies

- Savings and investments: Contributions to savings accounts, retirement funds, or investment accounts

Often Overlooked Expenses

- Cash withdrawals (where does the cash actually go?)

- Small recurring subscriptions (streaming, apps, memberships)

- Fees (ATM fees, service charges, late payment penalties)

- Gifts and donations

- Maintenance costs (car, home, electronics)

The goal is not to track every penny with obsessive precision. It is to capture enough data that your spending picture is accurate within a reasonable margin. If you miss a $2 coffee once a week, your monthly totals will still be useful. If you miss $200 in cash spending every month, they will not.

How Often Should You Track Expenses

The short answer: as close to real-time as possible.

The longer answer depends on your method. If you are tracking manually, logging expenses at the end of each day works better than trying to remember a week's worth of transactions on Sunday evening. If you are using an AI-assisted app, logging each expense as it happens takes only a few seconds and eliminates the memory problem entirely.

Weekly reviews are valuable regardless of your tracking method. Set aside 10 to 15 minutes each week to review your categorized spending, spot any miscategorizations, and check whether you are on track with your budget. Monthly reviews provide the bigger picture: trends, category totals, and progress toward financial goals.

The key insight is that tracking frequency affects accuracy. Daily tracking captures 95 percent or more of your spending. Weekly recall-based tracking might capture 70 to 80 percent. Monthly attempts to reconstruct spending from memory are essentially guesswork.

Common Expense Tracking Mistakes

Tracking Without Reviewing

Recording expenses is only half the process. If you log everything but never look at the summaries, you have data without insight. Schedule regular reviews to actually examine where your money goes.

Using Too Many Categories

Twenty or thirty expense categories create confusion. Start with 8 to 12 broad categories and add subcategories only if you need finer detail for a specific area of spending. Most people need categories like housing, food, transportation, entertainment, health, and savings. That covers the majority of spending.

Quitting After Missing a Day

Perfection is not the goal. If you miss a day or a weekend of tracking, estimate what you spent and move on. A tracking record that covers 90 percent of your spending is infinitely more useful than no record at all. The biggest mistake is treating a small gap as a reason to abandon the habit.

Ignoring Cash Spending

If you withdraw $200 from an ATM, that is not a "$200 ATM" expense. That $200 was spent on specific things. Track the actual purchases, not just the withdrawal. If you cannot remember exactly how cash was spent, create a "cash, untracked" category so the total at least appears in your records.

Choosing the Wrong Tool

A tool that is too complex will be abandoned. A tool that is too simple will not provide useful insights. Match the tool to your actual behavior. If you will not open a spreadsheet daily, do not use a spreadsheet. If you value privacy, do not use a bank-linked app. Find the method that fits your life, not the method that looks best on paper.

How AI-Assisted Tracking Removes the Friction

The historical problem with expense tracking is sustainability. Studies and surveys consistently show that most people who start tracking expenses stop within the first month. The reason is rarely motivation. It is friction. Entering expenses manually is tedious, and the reward (better financial awareness) feels distant compared to the immediate cost (time and effort for every transaction).

AI-assisted tracking attacks this friction directly. Instead of filling out forms with amount, category, date, and merchant, you can type a quick phrase like "lunch 12.50" or snap a photo of a receipt. The AI parses the input, suggests a category, and presents a confirmation screen. The entire process takes under five seconds.

Finny is built around this principle. It uses AI to handle the parsing and categorization while keeping you in the decision loop. You confirm every entry, which maintains accuracy and awareness. But you skip the tedious data entry that makes traditional tracking unsustainable. The app also works offline, so you can log expenses anywhere, whether you are on the subway, traveling abroad, or simply in a location with poor connectivity.

This hybrid approach preserves the benefits of manual tracking (accuracy, awareness, privacy) while eliminating the primary reason people quit (friction). It is not fully automatic, and that is intentional. The brief moment of confirming each expense reinforces spending awareness in a way that passive bank syncing does not.

The Bottom Line

Expense tracking is the foundation of personal financial awareness. Without it, budgeting is guesswork, saving goals lack context, and spending habits remain invisible. The practice itself is simple: record what you spend, categorize it, and review it regularly.

The challenge has always been sustainability, not concept. People understand why tracking matters. They struggle with the daily effort of doing it. Modern AI-assisted tools like Finny address this by reducing each entry to a few seconds of effort while maintaining the accuracy and control that make tracking worthwhile.

You do not need a perfect system. You need a consistent one. Start with broad categories, track daily, review weekly, and choose a method that matches your actual habits rather than your ideal ones.

Common Questions About Expense Tracking

What is expense tracking in simple terms?

Expense tracking is the practice of recording every purchase you make, organizing those records into categories, and reviewing them to understand your spending patterns. It answers the question "where does my money actually go?"

How is expense tracking different from budgeting?

Expense tracking records what you have already spent. Budgeting plans what you intend to spend. Tracking provides the data that makes budgets realistic. Most financial advisors recommend starting with tracking because you cannot plan a budget without knowing your actual spending habits.

What is the easiest way to track expenses?

AI-assisted apps offer the lowest friction. You type a short description or scan a receipt, and the app handles categorization. This approach takes seconds per entry compared to minutes for manual methods. For a full comparison of methods, see our guide on the best way to track expenses.

Do I need to link my bank account to track expenses?

No. Privacy-first expense trackers like Finny let you log expenses manually or with AI assistance without connecting bank accounts. This approach gives you full control over your financial data while still providing categorization and analytics.

How long should I track expenses before seeing results?

Most people notice spending patterns within two to four weeks of consistent tracking. After one full month, you have enough data to create a realistic budget. After three months, you can identify seasonal patterns and longer-term trends.

Ready to start tracking expenses without the friction?

Download Finny to log expenses with AI-assisted text input, receipt scanning, or voice. No bank connections required, works offline, and gives you full control over your financial data.