Investing a large sum of money all at once can feel risky. Markets fluctuate daily, and the fear of buying at a peak keeps many people on the sidelines. What if there were a way to invest consistently without worrying about timing the market perfectly?

Dollar cost averaging is that strategy. It involves investing a fixed amount of money at regular intervals, regardless of market conditions. Instead of trying to predict the best moment to invest, you spread your purchases over time. This guide covers how dollar cost averaging works, its advantages and drawbacks compared to lump sum investing, and how tracking your recurring contributions alongside everyday expenses gives you a complete view of your finances. For a broader look at managing your money, see our guide on how to manage personal finances.

What Is Dollar Cost Averaging

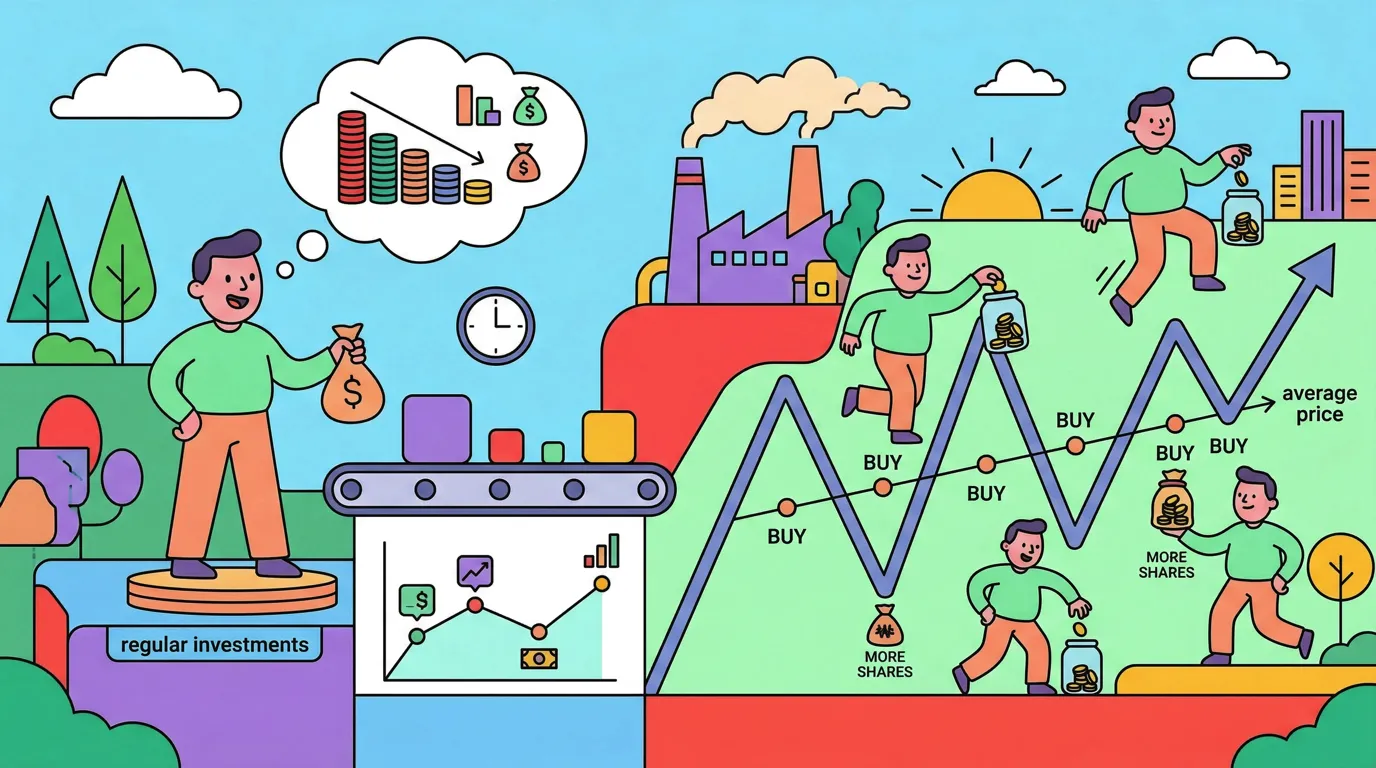

Dollar cost averaging (DCA) is an investment strategy where you invest a fixed dollar amount into an asset on a regular schedule, typically weekly, biweekly, or monthly. You buy more shares when prices are low and fewer shares when prices are high. Over time, this tends to lower your average cost per share compared to buying everything at a single high point.

The core principle is consistency over timing. Rather than analyzing charts and waiting for the "right" moment, you commit to a schedule and stick with it. Many people already practice dollar cost averaging without realizing it: contributing to a 401(k) or retirement account each paycheck is a classic example.

DCA works with virtually any investment: index funds, ETFs, individual stocks, or even cryptocurrency. The strategy is agnostic to the asset class. What matters is the discipline of regular, fixed-amount contributions.

How Dollar Cost Averaging Works: A Practical Example

Suppose you have $6,000 to invest in an index fund. You decide to invest $1,000 per month over six months instead of investing the full amount at once.

| Month | Share Price | Amount Invested | Shares Purchased |

|---|---|---|---|

| January | $50 | $1,000 | 20.00 |

| February | $45 | $1,000 | 22.22 |

| March | $40 | $1,000 | 25.00 |

| April | $42 | $1,000 | 23.81 |

| May | $48 | $1,000 | 20.83 |

| June | $52 | $1,000 | 19.23 |

Total invested: $6,000 Total shares purchased: 131.09 Average cost per share: $45.77

If you had invested the entire $6,000 in January at $50 per share, you would have purchased 120 shares. By using DCA, you ended up with 131.09 shares because you bought more when prices dipped in February, March, and April. Your average cost per share ($45.77) was lower than the starting price.

This is the mathematical advantage of DCA in a volatile market. You automatically buy more when prices are low, pulling your average cost down without any active decision-making.

Dollar Cost Averaging vs Lump Sum Investing

The debate between dollar cost averaging and lump sum investing is well-studied. Each approach has clear trade-offs.

When Lump Sum Wins

Research from Vanguard and other firms has shown that lump sum investing outperforms DCA roughly two-thirds of the time. The reason is straightforward: markets trend upward over long periods. If you have money available and the market goes up, waiting to invest means missing gains. Every month you hold cash instead of investing, you lose potential returns.

If you receive a windfall, an inheritance, a bonus, or proceeds from selling property, and you have a long time horizon, lump sum investing has the statistical edge.

When Dollar Cost Averaging Wins

DCA outperforms lump sum investing when markets decline after your initial investment. If you invest everything in January and prices drop 20% by March, your entire balance takes that hit. With DCA, only your January contribution experiences the full decline, and your later contributions buy at lower prices.

More importantly, DCA wins on the behavioral side. Many people who plan to invest a lump sum never actually do it. They wait for a pullback, then wait more, then forget. DCA removes this paralysis. A scheduled contribution happens whether you feel confident about the market or not.

Quick Comparison

| Factor | Dollar Cost Averaging | Lump Sum |

|---|---|---|

| Historical returns | Slightly lower on average | Slightly higher on average |

| Risk reduction | Reduces timing risk | Full exposure immediately |

| Behavioral ease | High, automated and routine | Low, requires conviction |

| Best for | Regular income, risk-averse investors | Windfalls, long time horizons |

| Regret potential | Lower | Higher if market drops after |

The right choice depends on your situation. If you are investing from monthly income, DCA is the natural approach. If you have a lump sum and a long horizon, investing it all at once is statistically favorable, but only if you can handle the short-term volatility without panicking and selling.

When to Use Dollar Cost Averaging

DCA is not a one-size-fits-all strategy. It works best in specific situations.

Investing From Regular Income

Most people do not have large lump sums waiting to be invested. They earn money each month and need to allocate it between expenses, savings, and investments. DCA is the obvious fit here. You set a fixed investment amount, automate it, and let it run.

Entering Volatile Markets

If markets feel uncertain and you are hesitant to invest a lump sum, DCA provides a middle ground. You get your money working without the anxiety of going all-in at a potentially bad time. Understanding compound interest helps reinforce why getting invested sooner, even gradually, matters more than waiting for the perfect entry.

Building Long-Term Wealth

DCA aligns well with long-term goals like retirement. Consistent contributions over 20 or 30 years smooth out market volatility almost entirely. The difference between DCA and lump sum becomes negligible over very long periods. What matters is that you invest regularly and do not stop during downturns.

Learning to Invest

New investors benefit from DCA because it reduces the pressure of making one large, high-stakes decision. Starting with smaller, regular investments builds familiarity with market movements and investment mechanics before larger amounts are at play.

Common Dollar Cost Averaging Mistakes

Stopping During Downturns

The biggest mistake is pausing contributions when markets drop. Downturns are exactly when DCA provides the most value: you are buying shares at lower prices. Stopping during a decline and resuming after recovery means you miss the discounted purchases that lower your average cost.

Ignoring Fees

If each investment transaction carries a fee, frequent small investments can be costly. Ensure your brokerage or platform offers commission-free trades for your chosen investments, or adjust your frequency to reduce fee impact. Monthly contributions are generally more cost-effective than weekly ones if fees are involved.

Using DCA to Avoid a Decision

DCA should be a deliberate strategy, not an excuse for indecision. If you have a lump sum and a long time horizon, spreading it over 24 months purely out of fear is not DCA. It is procrastination with a schedule. A reasonable DCA period for a lump sum is 3 to 12 months.

Not Increasing Contributions Over Time

Your income will likely grow over the years. If your DCA contributions stay flat, your investment rate relative to income actually shrinks. Review your contribution amount annually and increase it when your budget allows. This pairs well with a solid budgeting strategy that accounts for both spending and investing.

Tracking Investment Contributions Alongside Expenses

Most people track spending and investing separately. Monthly expenses go into one app or spreadsheet, investment contributions go into a brokerage statement, and the two rarely connect. This creates blind spots.

Your DCA contributions are a recurring financial commitment, just like rent or utilities. When you track them alongside your expenses, you get a complete picture of where your money goes each month. You can see whether your investment rate is sustainable, whether it crowds out necessary spending, or whether you have room to increase it.

An expense tracking app like Finny lets you log investment contributions as a category alongside daily spending. This way, your monthly review shows not just what you spent on groceries and transportation, but also how much you directed toward building wealth. You see the full outflow in one place.

How to Track DCA in Your Expense App

- Create an investment category: Add a category like "Investments" or "DCA Contributions" in your tracking app

- Log each contribution: When your scheduled investment executes, log the amount as an outflow to that category

- Review monthly totals: During your monthly review, compare investment contributions against total income and spending

- Adjust as needed: If your expense data shows you are consistently underspending in some categories, consider redirecting that surplus to increase your DCA amount

This approach connects your investing habit to your spending habits. You stop thinking of investing as something separate from your budget and start treating it as a non-negotiable monthly line item, the same way you treat your phone bill or daily spending.

How Much Should You Dollar Cost Average

There is no universal answer, but a practical framework helps.

Starter level: Invest 10% of your take-home pay. If you earn $4,000 monthly after taxes, set up a $400 monthly DCA contribution.

Growth level: Invest 15-20% of take-home pay. This accelerates wealth building significantly, especially when combined with employer retirement matching.

Aggressive level: Invest 25% or more. This is realistic if your essential expenses are well-managed and you have already built an emergency fund.

The right amount depends on your expenses, debt obligations, and financial goals. The key is choosing an amount you can sustain without interruption. A consistent $300 per month beats an ambitious $800 per month that you pause after three months because it strained your budget.

The Bottom Line

Dollar cost averaging is a strategy built on consistency rather than prediction. You invest a fixed amount on a regular schedule, buying more shares when prices drop and fewer when prices rise. Over time, this reduces the risk of investing everything at an unfortunate moment.

DCA is not always the mathematically optimal approach. Lump sum investing has a slight historical edge. But DCA is reliable, easy to automate, and removes the emotional barriers that keep people from investing at all. For most people investing from regular income, it is the natural and practical choice.

The habit of regular contributions matters more than the entry point. Start with an amount your budget supports, automate it, and increase it as your income grows. Track those contributions alongside your expenses to maintain a clear view of your complete financial picture.

Common Questions About Dollar Cost Averaging

What is dollar cost averaging in simple terms?

Dollar cost averaging means investing a fixed amount of money at regular intervals, such as $500 every month, regardless of whether the market is up or down. Over time, this approach lowers the average price you pay per share.

Is dollar cost averaging better than lump sum investing?

Lump sum investing has slightly higher average returns historically because markets tend to rise over time. However, dollar cost averaging reduces timing risk and is easier to commit to psychologically. For regular income investors, DCA is the more practical approach.

How often should I invest with dollar cost averaging?

Monthly is the most common frequency. It aligns with pay cycles and keeps transaction costs manageable. Weekly or biweekly contributions work too, especially if your brokerage charges no fees. The key is consistency, not frequency.

Can I use dollar cost averaging with any investment?

Yes. DCA works with index funds, ETFs, mutual funds, individual stocks, and even cryptocurrency. It is most effective with broadly diversified investments like index funds, where long-term upward trends are well-established.

When should I stop dollar cost averaging?

DCA is typically a long-term strategy that continues until you reach your financial goal, such as retirement. You might adjust the amount over time, but stopping entirely during market downturns defeats the purpose. The strategy works best when maintained through full market cycles.

Ready to track your investment contributions alongside daily expenses?

Download Finny to log DCA contributions, categorize spending, and see your complete financial picture in one place. No bank connections required, with full control over your data.