How to Recover From an Overspending Vacation (Step-by-Step)

You are sitting at the airport gate on the way home. The flight is delayed. You open your credit card app, mostly out of habit, and the balance lands like a small punch. Three currencies, a foreign transaction fee you forgot existed, two ride-share charges from a night you barely remember, and a hotel hold that has not dropped off yet. The trip was good. The number is not.

This guide is about what to do next. Not the lecture, not the budgeting platitudes, just a clear sequence of steps that get you from dread to a working plan. How to recover from overspending on vacation is mostly an exercise in seeing the damage clearly, separating one-time costs from quiet new habits, and choosing a payback pace you can actually live with. We will also cover multi-currency reconciliation, since most vacation overruns include foreign card charges that distort the picture.

If overspending is a longer pattern for you, our guide on how to stop overspending is a good follow-up. For now, focus on the reset.

Step 1: Triage the Damage Without Judgment

The first instinct after a big trip is to either avoid the statement entirely or open it and spiral. Neither helps. The goal of triage is to count the damage, not to grade yourself for it.

Sit down somewhere quiet. Open every account that touched the trip: your main credit card, any travel card, your debit card, PayPal, Apple Pay history, Venmo or other peer apps. Write down or screenshot the post-trip balance on each. Add them up. That total, including the trip prepayments you made before leaving, is your true vacation cost.

Many people stop here because the number feels heavy. Push past that. The number itself is information. It does not become smaller by being ignored, and it does not become larger by being faced. Most post-trip overruns look worse on day one than they do on day three, once pending charges settle and refunds for cancellations come back.

A useful framing: this is a closing balance, not a verdict. Your future spending and earning is still up to you.

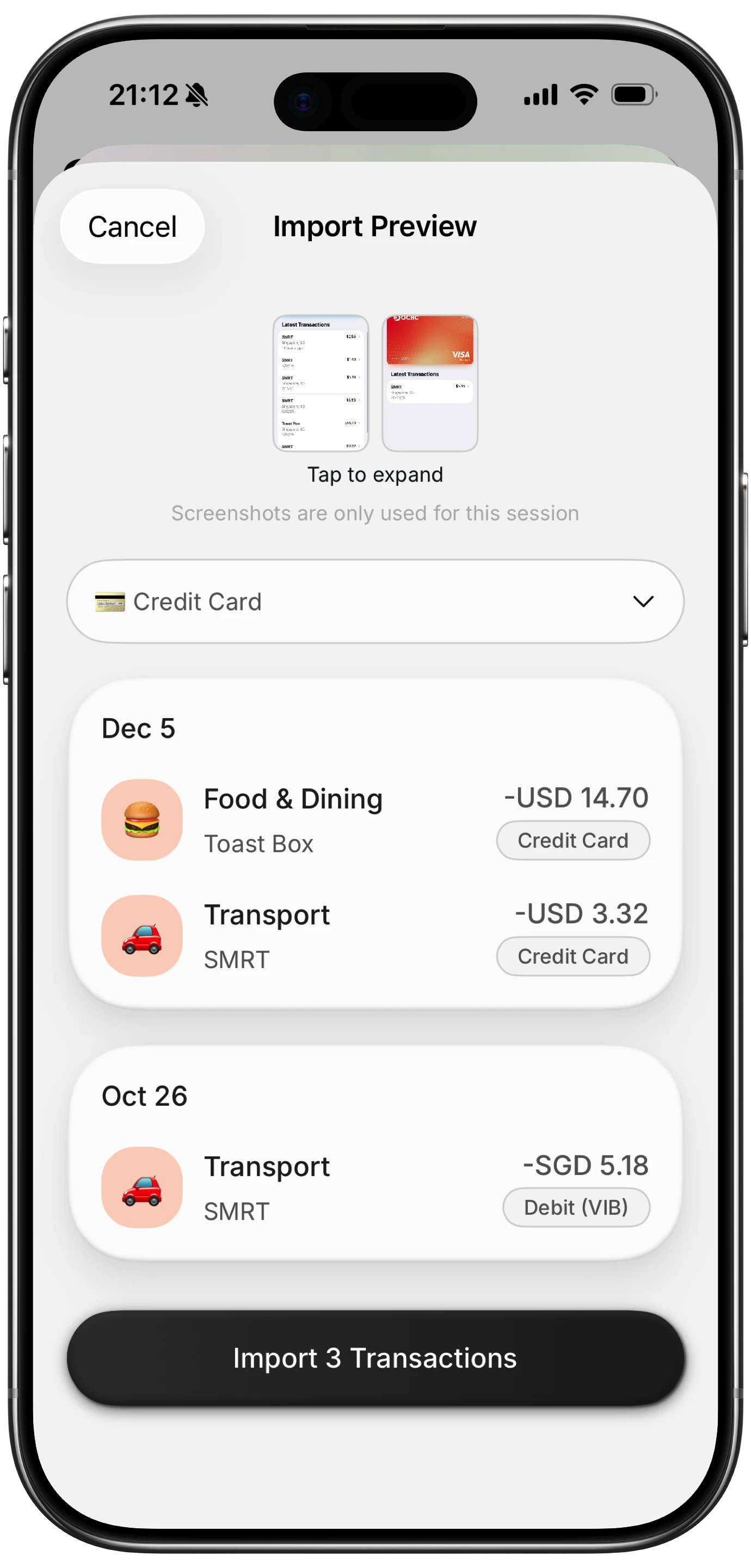

Step 2: Batch-Import Receipts and Pending Charges

Once you know the total, you need detail. Total damage tells you how much. Itemized detail tells you where, and that is what you need for everything that follows.

Pull out your phone, your wallet, and any folder of paper receipts you collected. Photograph the paper ones. Pull up email confirmations for hotels, tours, restaurants, and rentals. If you used a tool that captures receipts, this is where it earns its place. Apps with batch receipt scanning let you photograph a stack at once instead of one at a time, which is the difference between actually doing this step and putting it off for a week.

As you import, do not categorize yet. Just get every transaction into one place, with the date, merchant, original amount, and original currency. Cross-check each item against your card statements so you catch the charges that your memory missed: airport snacks, parking, the small bar tab on the last night.

By the end of this step you should have a single list of every vacation transaction. This is the raw material for the rest of the recovery.

Step 3: Reconcile Multi-Currency Charges

Vacation budgets quietly break on the currency line. You see a 4,200 yen dinner in your head, but your statement shows a slightly different dollar figure because of the conversion rate, and a separate foreign transaction fee on the next line. Multiply that by twenty meals and a few taxis and the gap between what you thought you spent and what your card actually charged can be ten percent or more.

To reconcile travel expenses properly, log each transaction in both its original currency and your home currency. Keep the original amount as your memory anchor. Use the home-currency amount for totaling. A unified currency view does this work for you: each line stays in the local currency, but the running total converts automatically so you can see the trip in one number.

While you reconcile, watch for three common surprises:

- Foreign transaction fees of around 1 to 3 percent that some cards charge per swipe.

- Dynamic currency conversion, where a merchant offers to charge you in your home currency at a worse rate than your card would give you.

- ATM withdrawal fees, which are often a flat fee plus a percentage and rarely show in your daily mental math.

Add these into the right line items so you understand the true cost of each category, not just the headline number.

Step 4: Separate One-Time Vacation Costs From Lifestyle Creep

This is the most important step in the entire recovery, and the one most people skip. Not all of the damage is vacation damage. Some of it is new habit damage that started on the trip and is about to follow you home.

Sort your itemized list into three buckets:

- One-time trip costs: flights, hotels, tours, visa fees, the rental car, travel insurance. These are real, but they are not recurring.

- Vacation lifestyle: restaurants instead of cooking, ride-share instead of transit, premium coffees, gift shopping, late-night drinks. These are habits you adopted because you were on holiday.

- New subscriptions or upgrades: the airport lounge membership you signed up for, the streaming service you added for the long flight, the premium SIM data plan that auto-renews, the upgraded credit card with a fee.

Bucket one is the cost of the trip. You knew it was coming. Bucket two is the part that often hides as "vacation spending" but is really just expensive defaults you fell into. Bucket three is the silent killer, because it keeps charging you next month even though the trip is over.

Cancel anything in bucket three you do not need. Then look at bucket two and decide which behaviors are coming home with you. A few might be worth keeping. Most are not. If you find yourself still ordering delivery every night two weeks later, the trip did not cause that, the trip just gave you permission to start.

Step 5: Build a 30, 60, 90 Day Recovery Plan

Now you have a clean number and a clean list. Time to plan the payback. The mistake here is trying to repay everything in one heroic month. That works for about ten days, then collapses, then leaves you worse off than if you had planned a calmer pace.

Use a 30, 60, 90 day frame:

- Days 1 to 30: Stabilize. No new discretionary debt. Pause non-essential subscriptions. Move to a stricter weekly grocery and dining number. Schedule the largest possible payment your real budget can handle without missing rent, utilities, or minimums. Some people slot in two or three no-spend days per week here as a circuit breaker.

- Days 31 to 60: Pay down. Now that your baseline is calmer, direct any windfalls (tax refund, bonus, side income) at the highest-interest balance from the trip. Keep dining and entertainment at the reset level. Resist the urge to celebrate hitting milestones with spending.

- Days 61 to 90: Rebuild. Once the trip balance is gone or close to gone, rebuild any savings buffer you tapped, especially your emergency fund. This is also the moment to start a small "next trip" sinking fund so the next vacation is paid for in advance, not paid off after.

Write the plan down. A plan that lives only in your head will quietly negotiate itself smaller every week.

Step 6: Decide Whether to Cut, Earn, or Stretch

Recovery has three levers. Cut spending. Earn extra income. Stretch the payback period. Most people instinctively reach for the first one because it feels the most virtuous. In practice, the right answer is usually a blend.

Cutting works if your trip overrun was modest, maybe a few hundred to a thousand dollars, and you have obvious slack in your monthly budget. Cancel two streaming services, drop dining out for a month, and you are done. For larger overruns, pure cutting tends to hit a wall. There is only so much you can carve out of a real life before the cuts feel like punishment, and punishment plans do not last. If you want a sharper version of cutting for a defined period, a spending fast is one structured option.

Earning is underused. A short freelance gig, selling unused gear or clothes, picking up extra shifts, or rerouting a tax refund or bonus toward the trip balance can clear hundreds or thousands faster than cutting can. Even a one-time effort that closes 30 percent of the balance changes the emotional weight of the rest.

Stretching, meaning paying it off over four to six months instead of one or two, is fine if the interest rate is reasonable and you are realistic about the cost. It is not fine if the balance is sitting on a 24 percent credit card. In that case, look at a 0 percent balance transfer offer or a lower-rate personal loan, run the math honestly, and pick the path that minimizes total interest.

Step 7: Set Up a Better System Before the Next Trip

The point of all this is not to feel bad about the last vacation. It is to make the next one easier. A few small system changes prevent most of the damage you just cleaned up.

Open a dedicated travel sinking fund and automate a monthly transfer into it. Even fifty dollars a month means six hundred dollars of paid-for trip per year. Set a per-day spending target before the next trip and write it on the inside of your luggage tag if you have to. Use a card with no foreign transaction fee. Track expenses on the trip itself, not after, so the running total is always visible. A travel budget app makes this much less painful than a spreadsheet on a phone screen.

If you are reading this because the multi-currency mess is what hurt the most, it is worth considering a tracker that handles original currency and home currency in one view, and that lets you batch-import receipts in a few minutes instead of an evening. Finny does both, alongside offline tracking that works on planes and in basements with no signal, for $1.99 a month and no bank login. Two or three minutes a day on the trip is far less work than two or three hours of recovery after.

The Bottom Line

A vacation overrun feels worse than it is, especially in the first 48 hours when pending charges are still settling and the credit card statement looks larger than the real damage. The recovery is not magic. Triage what you actually owe. Itemize it. Reconcile the foreign currency lines so the total is accurate. Separate the one-time costs from the new habits and subscriptions you accidentally signed up for. Build a 30, 60, 90 day plan. Mix cutting, earning, and a sane payback period. Set up a small system so the next trip does not become a next recovery.

You went somewhere. You came back. Now the work is just clean, boring, and finite.

Common Questions About Vacation Spending Recovery

How long should it take to recover from an overspending vacation?

Most people can recover from a moderate vacation overrun within 30 to 90 days, depending on the size of the balance and their monthly income. Smaller overruns of a few hundred dollars usually clear in one billing cycle if you cut a few discretionary categories. Larger overruns of one to three thousand dollars typically take two to three months when you combine spending cuts with extra income. Avoid stretching past six months on high-interest credit, since interest costs start to dominate the balance.

What is a post vacation budget reset?

A post vacation budget reset is a short, structured exercise to get your spending back on track after a trip. It usually involves three things: counting the true total damage across every account you used, separating one-time trip costs from new lifestyle habits the trip created, and resetting weekly grocery, dining, and entertainment numbers to a stricter baseline for 30 days. Done well, it takes about an hour and prevents the holiday spending hangover from quietly extending into a permanent lifestyle increase.

How do I reconcile travel expenses across multiple currencies?

Log each transaction in its original currency to keep the merchant amount intact, then convert to your home currency for totals. Use your card statement as the source of truth for the actual converted amount, since that includes any foreign transaction fees and the exact exchange rate your card used. A unified currency view in a tracker app does this automatically. Watch for dynamic currency conversion at point of sale, ATM fees, and the 1 to 3 percent foreign transaction fees some cards charge.

Should I use savings or a payment plan to clear vacation debt?

It depends on the interest rate. If the vacation balance is on a credit card charging 18 to 25 percent and you have savings beyond your emergency fund, paying it down with savings is almost always cheaper than letting it accrue interest. If clearing it would empty your emergency fund, do not. A 0 percent balance transfer card or a lower-rate personal loan is usually a better option than carrying high-interest credit card debt for months. Rebuild savings as the next priority once the balance is cleared.

How do I avoid overspending on the next vacation?

Set a per-day spending target before you leave, open a sinking fund and pre-fund as much of the trip as possible, and use a card with no foreign transaction fee. On the trip itself, log expenses the same day rather than at the end of the week, so the running total stays visible. Batch-scan receipts every few nights instead of letting them pile up. Most overruns happen in the last third of a trip, when fatigue erodes tracking discipline, so build in a mid-trip check-in to reset.

Ready to take the dread out of the next post-trip statement?

Download Finny to log expenses using AI text, voice, or batch receipt scanning, with a unified currency view that reconciles foreign card charges automatically. No bank connections, offline support, and full control over your financial data.