How to Budget When Your Paycheck Changes Every Month

A salaried worker opens a budget app, types in one number, and the math is done for the next two weeks. A freelance designer, a DoorDash driver, a hairstylist who lives on tips, or a sales rep on commission cannot do that. Their income arrives in lumps. One week is $1,400, the next is $380, and the month after that they invoice $6,200 because three projects closed at once. Standard 50/30/20 advice does not survive contact with that kind of pay schedule.

This guide walks through a 4-step method for how to budget on variable income without spreadsheets that fall apart the moment a client pays late. The same approach works for irregular income budgeting whether you are a freelancer, a gig worker, a tipped employee, or a commission earner. We will cover how to build a floor, how to pay yourself a steady "salary," how to size a buffer fund, what to do with windfall months, and the self-employment tax piece that catches most first-year freelancers off guard. For a refresher on the basics before diving in, the how to budget money guide is a good starting point.

Why standard budgeting advice fails on variable income

Most budget templates assume two predictable inputs and a list of fixed outputs. Variable income breaks the input side. If you build a budget around an "average" month and the month comes in 30 percent below average, you are short rent before the second week. If you build it around a worst-case month and the month comes in 40 percent above average, you have no plan for the surplus and it disappears into restaurants and impulse buys.

Variable income also makes zero-based budgeting harder, because you cannot assign every dollar a job at the start of the month if you do not yet know how many dollars you will have. The fix is not to abandon zero-based thinking. The fix is to separate the act of earning from the act of spending. Earnings flow into a holding account. Spending is funded by a fixed monthly transfer from that holding account. The buffer between the two is what makes the system stable.

Step 1: Calculate your true baseline expenses

Before you can pay yourself anything, you need to know the floor. Baseline expenses are the bills you must cover every month to keep the lights on, the roof intact, and the work going. Be honest and granular. Open the last three months of your bank and card statements and add up:

- Rent or mortgage

- Utilities, including phone and internet

- Insurance: health, auto, renters, disability

- Minimum debt payments

- Groceries, calculated as your real monthly average not your aspirational figure

- Transportation: gas, transit, vehicle maintenance, tolls

- Childcare or dependent care

- Subscriptions you will not cancel this quarter

- Business costs that recur: software, accountant, mileage, supplies

Add it up. That number is your floor. For a single freelancer in a mid-cost city, this is often somewhere between $2,400 and $3,800 per month. For a family with one variable earner, it can run $5,000 to $8,000. Write the number down. This is the minimum you must clear, after taxes, every single month. If you also want to understand which line items can flex when things get tight, the explainer on what is a variable expense will help you separate fixed obligations from things you can cut.

Step 2: Apply the lowest-month rule to set your "salary"

Here is the central move. Look back at your last 12 months of income. If you do not have 12 months yet, use 6. Find your worst month, the one where the deposits were smallest. Say your worst month was $2,800 net after platform fees and refunds. That number, or something close to it, becomes the monthly "salary" you pay yourself from a holding account into your spending account.

The logic: if your worst real-world month is $2,800 and your baseline expenses are $2,600, you have a sustainable floor. You can pay yourself $2,800 every month and meet your obligations even in a bad stretch. Better months pile up surplus in the holding account, which feeds the buffer and the windfall buckets we cover next.

If your worst month is below your baseline, you have two options and you must pick one. Option A: cut the baseline until it fits. Cancel subscriptions, renegotiate insurance, downsize housing at renewal, refinance debt. Option B: raise the floor by adding a stabilizing income source, such as a part-time anchor job, a retainer client, or a gig with predictable hours. There is no third option that involves wishful thinking. A budget that requires every month to be average is not a budget, it is a hope.

Set up two checking accounts at the same bank or credit union. Call one "Income" and the other "Spending." All client payments, gig deposits, tips, and commissions land in Income. On the first of every month, you transfer your fixed salary from Income to Spending. This is the freelancer-friendly cousin of the pay yourself first principle, applied to your operating cash rather than just your savings.

Step 3: Build a buffer fund for shortfall months

The lowest-month rule works only if you have a buffer to absorb the months that come in even lower than your historical worst. Markets shift, clients churn, gig platforms cut rates, you get sick, a snowstorm kills two weeks of restaurant tips. The buffer is what lets you keep paying yourself the same salary while income recovers.

Aim for a buffer of two to three months of your salary, parked in the Income account or a linked high-yield savings account. If your salary is $2,800, the buffer target is $5,600 to $8,400. This is separate from a full emergency fund covering job loss or medical events. The buffer is for normal income volatility. The emergency fund sits behind it.

You build the buffer using surplus from good months. Until the buffer hits its target, every dollar above your salary stays in the Income account or savings. No exceptions. Once the buffer is funded, you can move on to the windfall system in step 4. If the buffer concept is new to you, the how to build an emergency fund fast and smart guide walks through a similar approach for a deeper rainy-day reserve.

In the first 90 days of running this system, expect things to feel tight. You are paying yourself a conservative number while also trying to build a buffer. Most people who switch to this method describe months one through three as bumpy. Months four through six is when the buffer starts doing real work and the anxiety drops noticeably.

Step 4: A percentage system for windfall months

Once the buffer is funded, you need a rule for what to do with the extra cash that piles up in good months. Without a rule, the surplus quietly migrates into lifestyle inflation. With a rule, every windfall dollar gets a job before you see it.

A starting allocation that works for most variable earners:

- Taxes set-aside: 25 to 30 percent

- Long-term savings or retirement: 20 percent

- Buffer top-up if it has been drawn down: 10 percent

- Annual or quarterly bills sinking fund: 10 percent

- Debt payoff above the minimum: 15 percent

- Discretionary, guilt-free spending: 15 to 20 percent

Run those percentages every time you see a deposit hit the Income account that pushes you above your salary plus the buffer target. Move the money the same day. Five minutes of action prevents weeks of drift.

The discretionary slice matters. If the system has zero reward in good months, you will abandon it. A 15 to 20 percent splurge bucket lets you take the trip, upgrade the laptop, or eat out without breaking the structure. The other 80 percent is doing the heavy lifting in the background.

Self-employment taxes: the piece nobody warns you about

If your variable income comes from 1099 work, gig platforms, or your own business rather than a W2 job, no one is withholding taxes for you. The rough rule of thumb is to set aside 25 to 30 percent of every net deposit for federal income tax, state tax if applicable, and the 15.3 percent self-employment tax that covers Social Security and Medicare. Some high-earning freelancers in high-tax states need closer to 35 percent.

Move the tax money into a separate savings account the same day income arrives. Treat it as not yours. The IRS expects quarterly estimated payments in April, June, September, and January. Missing them triggers penalties and interest. If you are unsure whether you owe self-employment tax or how 1099 income differs from a paycheck, the W2 vs 1099 breakdown covers the basics. For a tracking workflow built specifically around this kind of income, see the self-employed expense tracker for iPhone guide.

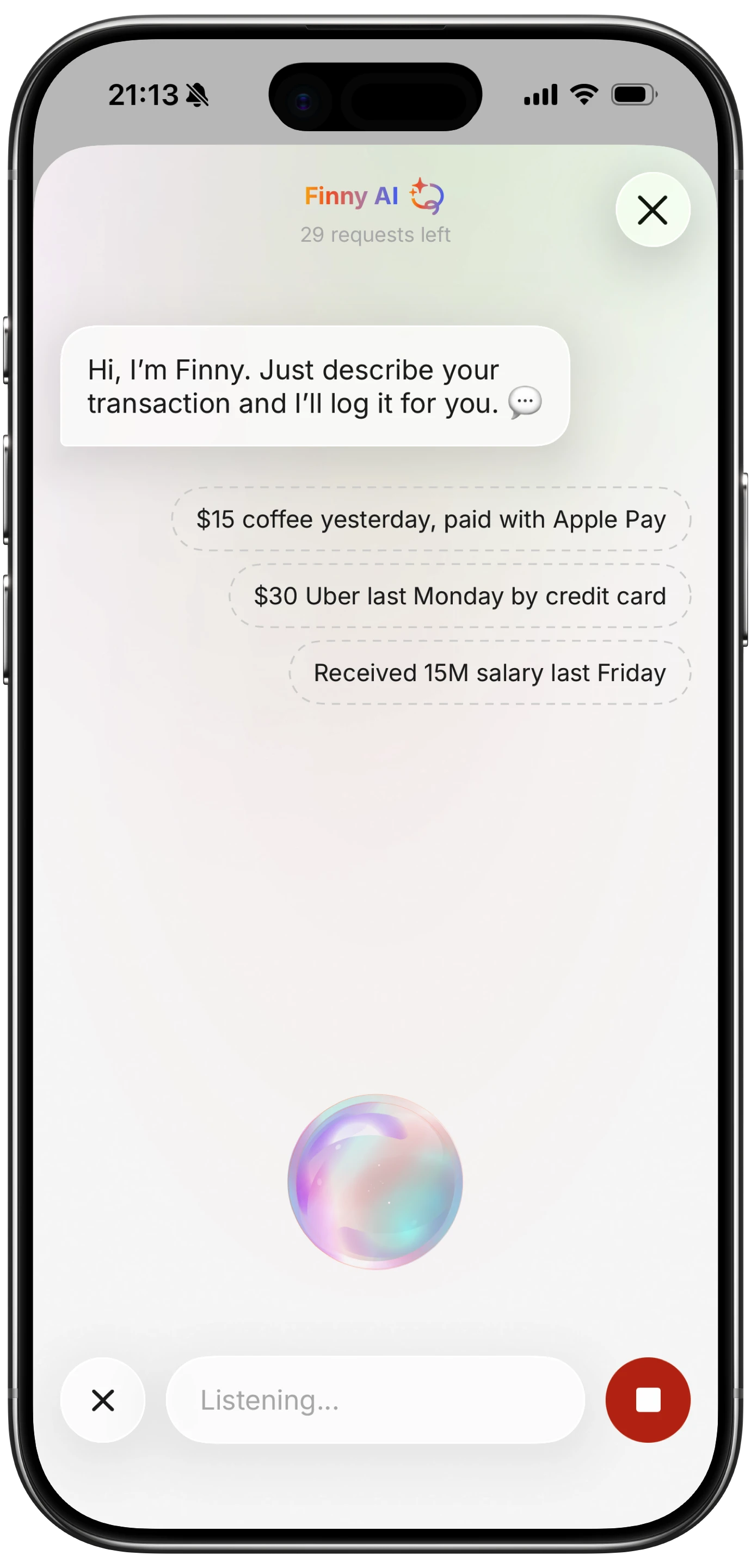

How to log income and expenses without losing momentum

The hardest part of variable income budgeting is not the math. It is the logging. A rideshare driver finishing a 9-hour shift is not opening a spreadsheet at 2 a.m. A freelance editor between two client calls is not categorizing a coffee receipt by hand. If logging takes more than a few seconds, it does not happen, and the system collapses two weeks in.

This is where Finny earns its place in the workflow. Voice input lets a gig worker hold a phone, say "twenty-two dollars gas at Shell," and have the expense logged before the pump finishes. Receipt scanning batches a stack of business meal receipts into entries in under a minute. Custom categories let you build tax-aware buckets like "1099 expenses: software," "1099 expenses: mileage," and "1099 expenses: meals" so that quarterly tax prep is a filter, not an archaeology dig.

The dashboard view also matters when income swings. Seeing a month-to-month column chart of income against baseline expenses tells you, at a glance, whether the buffer is doing its job or starting to drain.

Finny is $1.99 per month for Pro, works offline so a dead zone in a delivery van does not stop you from logging, and never asks for a bank login. The free tier covers unlimited manual tracking and custom categories if you want to test the workflow first.

A worked example: the freelance designer

Make this concrete. Maya is a freelance brand designer. Her last 12 months of net income, after platform fees, looked like this:

- Worst month: $3,100

- Best month: $9,400

- Average month: $5,800

- Baseline expenses: $2,900

She sets her salary at $3,100. Every first of the month, $3,100 transfers from Income to Spending. In her best month, $9,400 lands. After the $3,100 salary transfer, $6,300 stays in Income. She moves $1,890 to a tax savings account, $1,260 to retirement, $630 to her annual-bills fund, $945 to extra debt payoff, and $1,260 to her "good month" discretionary bucket. Nothing sits unassigned.

Over a year, the worst three months drain about $1,800 from her Income buffer because she still pays the $3,100 salary even when the deposit is below it. The good months refill that buffer multiple times over. By month nine, her buffer is fully funded at $9,300 and she is putting full windfall percentages to work. By month twelve, her tax bill is fully covered before she files.

Common Questions About Budgeting on Variable Income

How do I budget on variable income if I have less than 6 months of data?

Use what you have and rebuild as data accumulates. With three months of data, set your salary at the lowest of those three months minus 10 percent for safety. Recalculate every month for the first year. Keep a small written log of every deposit so you have clean data when it is time to reset your salary number. Avoid setting the salary based on a single great month. New freelancers often anchor on their best week and run out of cash by month two.

What is the best irregular income budget method for gig workers?

The 4-step method in this guide adapts well to gig work. Drivers, couriers, and shoppers should treat each platform deposit as net of a 25 to 30 percent tax holdback before counting it. Mileage, phone use, and supplies are deductible, so log them in real time. A short voice note after every shift is faster than batching at week's end. Set the salary at your worst recent month, build a buffer of at least one month of expenses before relaxing, and reserve windfall percentages for tax, savings, and debt.

How much should a freelancer save for taxes?

A safe starting estimate is 25 to 30 percent of net income set aside for federal income tax plus the 15.3 percent self-employment tax. Higher earners and residents of high-tax states should plan closer to 30 to 35 percent. Move the money the same day income arrives, into a separate savings account you do not touch. Make quarterly estimated payments to the IRS to avoid underpayment penalties. A tax professional is worth the fee in the first year of self-employment.

What if my baseline expenses are higher than my worst income month?

You have a structural shortfall, not a budgeting problem. Cut the baseline first. Cancel non-essential subscriptions, shop insurance, refinance debt, downsize at the next lease renewal. If cutting cannot close the gap, add a stabilizing income source: a part-time anchor job, a retainer client, or a regular shift on a predictable platform. A budget cannot solve a math problem where outflows exceed the worst-case inflow. Fix the inputs before refining the system.

How long until variable income budgeting feels normal?

Most people report the first 90 days as bumpy. The buffer is still small, every shortfall month feels personal, and the discipline of moving windfall percentages on the same day takes practice. By month four to six, the buffer is doing real work and the anxiety drops. By month nine to twelve, the system runs in the background and you stop noticing income volatility the way you used to. Patience in the first quarter is the price of stability for the rest of the year.

Ready to track expenses with less friction?

Download Finny to log expenses using AI, receipts, or voice. No bank connections, offline support, and full control over your financial data, for $1.99 per month.