How Compound Interest Works (With Examples)

Most people know that money "grows over time," but fewer understand the actual mechanism behind it. How compound interest works is one of the most useful things you can grasp about personal finance, because the math is simple once you see it in action. This post walks through the mechanics step by step, shows you real numbers at multiple time horizons, and explains the levers you can pull to make the effect work harder for you. For the underlying formula and its derivation, see our post on what compound interest is and how the formula works.

How Compound Interest Works

Compound interest is the process by which interest earned on a principal balance is added back to that balance, so future interest is calculated on a larger amount. Each compounding period you earn interest on your original deposit plus every dollar of interest you have already accumulated. Over time this creates a snowball: the balance grows, the interest payment grows, the balance grows again.

That is the core mechanic. The contrast is simple interest, where you earn the same fixed dollar amount every period because the base never changes. Compound interest breaks that ceiling.

To make this concrete: if you deposit $1,000 at 5% annual interest, compounded annually, you earn $50 in year one. In year two you earn 5% of $1,050, which is $52.50. In year three you earn 5% of $1,102.50, which is $55.13. The dollar amount of interest rises every single year without you adding a cent. That acceleration is what people mean when they call compound interest "interest on interest."

Worked Examples: What the Numbers Actually Look Like

Reading about compounding is one thing. Seeing the numbers is another. The table below shows a single $10,000 deposit at 5% annual interest, compounded annually, left untouched. No additional contributions.

| Year | Balance | Interest Earned That Year | Total Interest Earned |

|---|---|---|---|

| 0 | $10,000 | $0 | $0 |

| 5 | $12,763 | $607 | $2,763 |

| 10 | $16,289 | $776 | $6,289 |

| 20 | $26,533 | $1,264 | $16,533 |

| 30 | $43,219 | $2,058 | $33,219 |

A few things to notice:

- The dollar amount earned each year almost triples from year 5 to year 30, even though the deposit never changed.

- After 30 years the account has earned more than three times the original deposit in interest alone.

- The balance between year 20 and year 30 grows by more than $16,000, which is more than the entire original deposit.

That last point captures why time is the most powerful variable in this equation.

A second scenario: monthly contributions

Now assume a smaller starting point of $1,000, with $200 added every month at 5% annual interest compounded monthly.

| Year | Total Contributed | Balance | Interest Earned (Total) |

|---|---|---|---|

| 5 | $13,000 | $14,657 | $1,657 |

| 10 | $25,000 | $31,792 | $6,792 |

| 20 | $49,000 | $82,551 | $33,551 |

| 30 | $73,000 | $167,688 | $94,688 |

After 30 years the account holds nearly $168,000 against $73,000 contributed. The gap, nearly $95,000, is pure compounding. And the rate of that gap widening accelerates as time passes.

What Changes the Outcome

Four variables control how fast a balance grows under compound interest. Understanding each one lets you make deliberate decisions rather than guessing.

Time

Time is the variable with the largest effect by a wide margin. Because each period's interest becomes the base for the next period's calculation, longer time horizons produce disproportionately large results. Starting five years earlier can be worth more than doubling your monthly contributions. This is the core argument for dollar-cost averaging into investments as early as possible rather than waiting for a "perfect moment."

Interest rate

A higher rate multiplies every dollar faster. At 4% annually, $10,000 grows to roughly $32,434 after 30 years. At 6%, the same deposit grows to $57,435. That two-percentage-point difference produces an extra $25,000 over three decades. This is why finding a high-yield savings account that pays 4-5% APY, rather than a standard account paying 0.01-0.5%, matters so much for cash savings. As of mid-2026, the best high-yield savings accounts are offering up to 5.00% APY.

Compounding frequency

The same annual rate produces different results depending on how often interest is applied. Compounding quarterly beats compounding annually. Compounding monthly beats quarterly. Compounding daily beats monthly. The differences are smaller than most people expect at moderate rates, but they compound the same way the interest does: they add up over long periods.

For example, $10,000 at 5% for 30 years:

- Compounded annually: $43,219

- Compounded monthly: $44,812

- Compounded daily: $44,880

The monthly-vs-daily gap is small. The annual-vs-monthly gap is meaningful.

Additional contributions

Regular contributions amplify the compounding effect because every new dollar you add immediately starts earning interest on itself. Even modest monthly amounts, added consistently, can dwarf the impact of a larger lump sum invested once and left alone. The second table above illustrates this: $200 a month turns a $1,000 starting balance into nearly $168,000 over 30 years.

This principle is also central to strategies like index fund investing and the mechanics behind the 4% rule, both of which assume compounding growth over long periods.

How to Calculate It and Use a Calculator

The compound interest formula written as plain text is:

A = P(1 + r/n)^(nt)

Where:

- A is the final balance

- P is the principal (starting amount)

- r is the annual interest rate as a decimal (5% = 0.05)

- n is the number of compounding periods per year (12 for monthly, 365 for daily)

- t is the number of years

You can work through this manually for a single scenario, but a calculator handles it faster, especially when you want to compare multiple combinations of rate, time, and contribution amount.

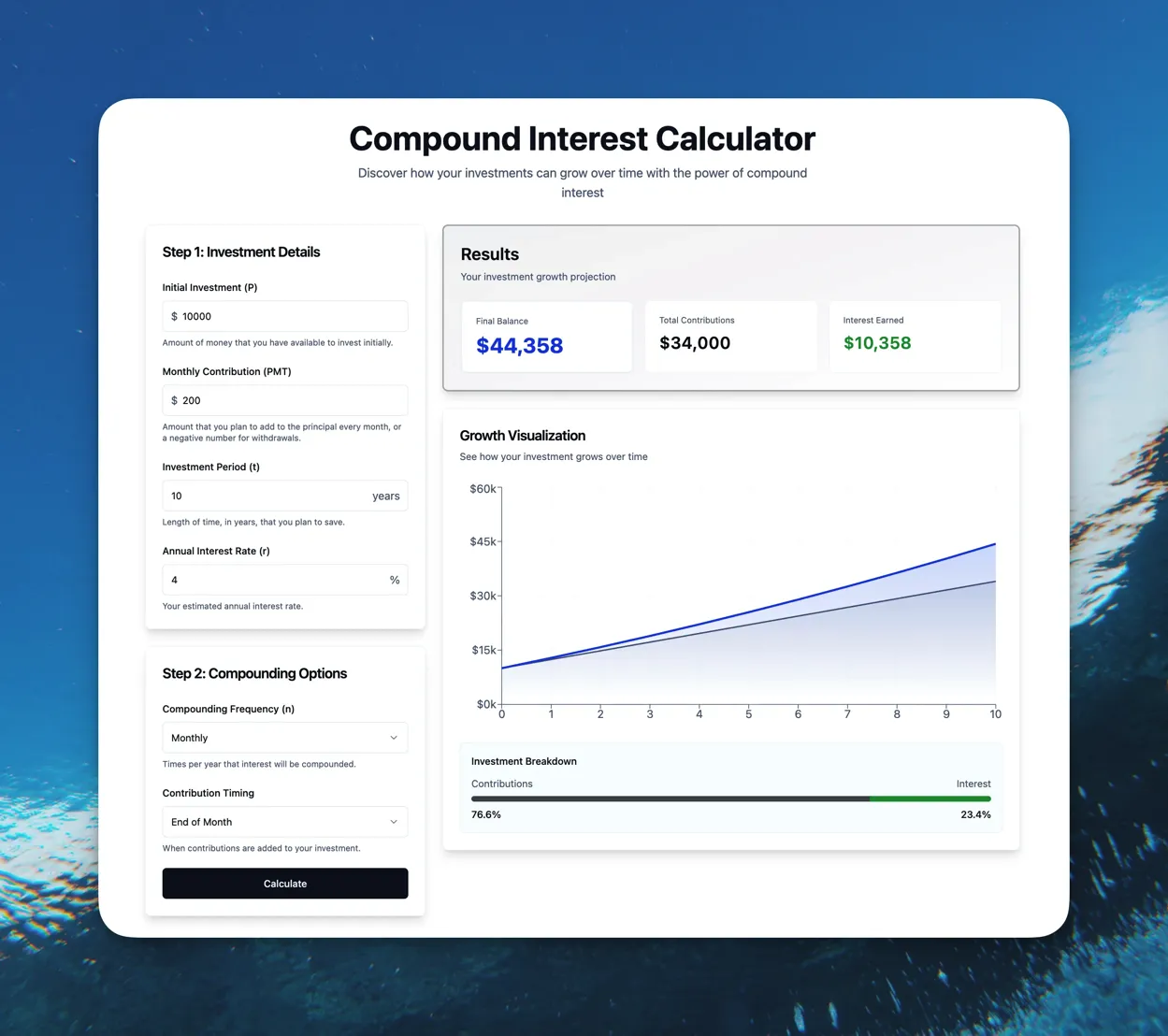

Finny's free compound interest calculator lets you set a starting balance, a monthly contribution, an annual rate, compounding frequency, and time horizon. You can adjust any variable and immediately see how the balance and interest earned change. It is useful both for planning savings goals and for building an intuition for how each lever affects the outcome.

For a full breakdown of the formula, including how to derive it and how to adjust it for regular contributions, see the companion post on compound interest: definition and formulas.

The Bottom Line

Compound interest is not a trick or a shortcut. It is a mathematical property of reinvesting returns. The mechanics are straightforward: interest earns interest, the balance grows, and the process repeats. The effect is modest over short periods and dramatic over long ones.

The clearest takeaways from the examples above:

- Start early. Time is the variable you can least replace.

- Use a competitive rate. A few percentage points make tens of thousands of dollars of difference over 30 years.

- Contribute regularly. Consistent additions accelerate the snowball.

- Check compounding frequency. Monthly or daily compounding beats annual at the same stated rate.

If you track your savings and net worth in Finny, you can watch these balances compound in real time, without connecting a bank account and without your data leaving your device.

Ready to put compound interest to work? Use Finny's free compound interest calculator to model your scenario, then download Finny to track your progress privately, on your own terms.

Common Questions About Compound Interest

How does compound interest work?

Interest is calculated on the current balance, not just the original deposit. Each time interest is added, the balance increases, so the next interest calculation produces a larger dollar amount. This cycle, where interest earns interest, is what makes balances grow faster over time. The longer you let the process run, the larger the effect relative to the starting amount.

What is the compound interest formula?

The standard formula is A = P(1 + r/n)^(nt), where P is the principal, r is the annual rate as a decimal, n is compounding periods per year, t is years, and A is the final balance. For a step-by-step explanation of how this formula is derived and how to adjust it for regular contributions, see our post on compound interest definition and formulas.

How often does interest compound?

It depends on the account or investment. Savings accounts typically compound daily or monthly. Bonds often compound semi-annually. Many investment returns are modeled as compounding annually for simplicity. More frequent compounding produces a slightly higher effective yield at the same stated annual rate, because interest starts earning interest sooner.

Is compound interest good or bad?

It depends on which side of the equation you are on. For savings and investments, compound interest works in your favor: your balance grows faster the longer you wait. For debt, especially credit card debt, the same math works against you: unpaid balances accumulate interest, which then accrues more interest. The mechanics are identical; the outcome depends on whether you are the lender or the borrower.

Does compound interest work the same for investments as for savings accounts?

The principle is the same, but the mechanics differ. Savings accounts pay a stated APY and compound on a fixed schedule. Investment returns vary by year and are not guaranteed. When analysts model long-run stock market growth, they use compound annual growth rates (CAGRs) as approximations. Historically, broad index funds have produced long-run average returns in the range of 7-10% annually before inflation, but past performance does not predict future results. See our post on index funds for more detail.